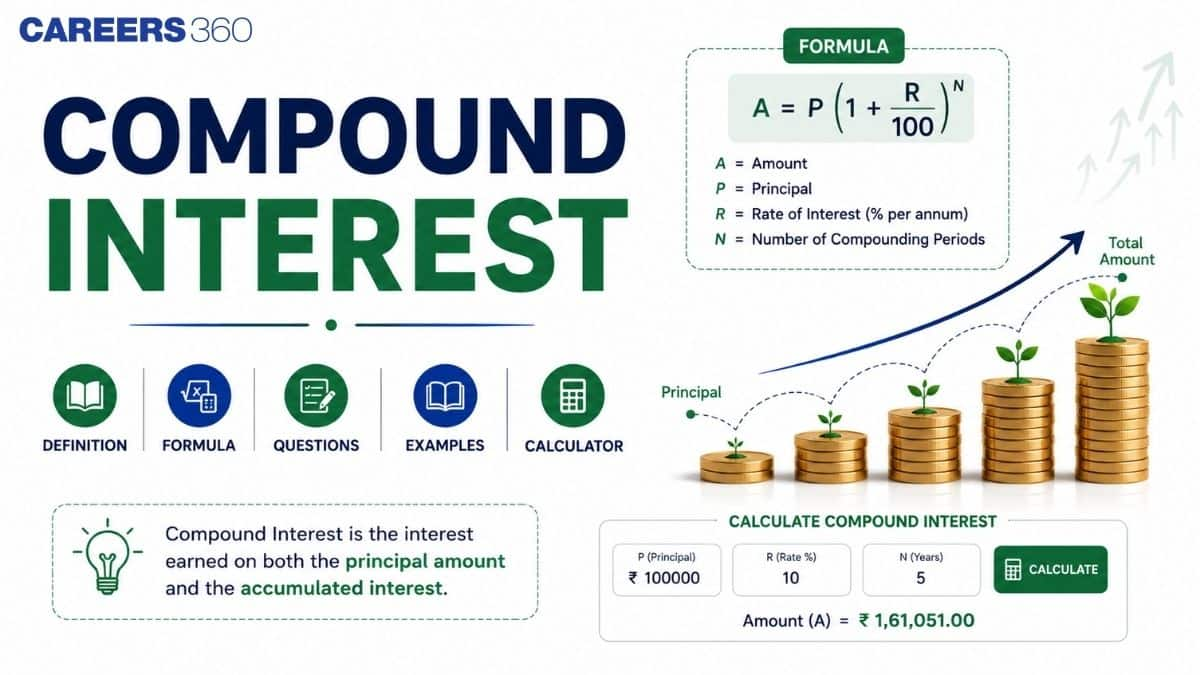

Compound Interest: Definition, Formula, Question, Examples, Calculator

Compound interest is something many of us experience in real life without always noticing it. For example, if you keep ₹10,000 in a savings account, the bank gives you interest on it. But from the next year, you start earning interest not just on ₹10,000, but also on the interest already added to it. This “interest on interest” is called compound interest, and that’s why your money grows faster over time. In Mathematics and quantitative aptitude, compound interest is an important topic because it combines percentages, exponents, and practical financial calculations. It is commonly asked in school exams, CBSE Class 8-10 Mathematics, competitive exams like SSC, Bank exams, CAT, CUET, and other aptitude tests. In this article, we will understand the meaning of compound interest, its formula, solved questions, real-life examples, and how to calculate it easily using a compound interest calculator.

This Story also Contains

- What is Compound Interest?

- Difference Between SI and CI for 3 Years

- Compound Interest Formula

- Derivation of the Compound Interest Formula

- How to Calculate Compound Interest if Interest is Compounded Half-Yearly?

- Applications of Compound Interest

- Best Books for Compound Interest

- Shortcut Tricks for Compound Interest

- Tips to Solve Compound Interest Questions Quickly

- Important Compound Interest Formula Table

- Solved Examples based on Compound Interest

- Related Quantitative Aptitude Topics

What is Compound Interest?

Compound interest is the interest calculated on both the original principal amount and the interest already added over previous periods. In simple words, it is interest earned on interest. Because of this, the money grows faster compared to simple interest, where interest is calculated only on the original principal.

In Mathematics, compound interest is an important chapter in profit and loss, percentages, and commercial maths. It is widely used in banking, savings accounts, fixed deposits, loans, investments, and insurance calculations.

The basic formula of compound interest is:

$A = P\left(1 + \frac{R}{100}\right)^n$

Where:

$P$ = Principal amount (initial money invested or borrowed)

$R$ = Rate of interest per annum

$n$ = Time period

$A$ = Final amount after interest

Then, $CI = A - P$ where $CI$ is the compound interest.

Compound Interest Meaning in Simple Words

The easiest way to understand compound interest is:

You invest some money.

You earn interest on it.

In the next period, interest is calculated on money + previous interest.

This keeps repeating, and the total amount grows faster every year.

That is why compound interest is often called “interest on interest.”

Key points to remember:

Compound interest increases the total amount faster than simple interest.

It depends on:

Principal amount

Interest rate

Time period

Number of times interest is compounded

Commonly used in bank deposits, recurring investments, and long-term wealth growth.

Real-Life Example of Compound Interest

Suppose you deposit ₹10,000 in a bank at 10% annual compound interest for 2 years.

Year 1:

Interest:

$I = \frac{10000 \times 10}{100} = 1000$

Amount after 1 year:

$A = 10000 + 1000 = 11000$

Year 2:

Now interest is calculated on ₹11,000:

$I = \frac{11000 \times 10}{100} = 1100$

Final amount:

$A = 11000 + 1100 = 12100$

So, $CI = 12100 - 10000 = 2100$

This shows that in the second year, you earned interest on the earlier interest too.

Where we see compound interest in daily life:

Savings bank accounts

Fixed deposits (FDs)

Mutual fund investments

Home loans

Education loans

Credit card outstanding balances

Difference Between Simple Interest and Compound Interest

Many students confuse simple interest vs compound interest. The main difference is how the interest is calculated.

| Basis | Simple Interest | Compound Interest |

|---|---|---|

| Interest calculated on | Principal only | Principal + previous interest |

| Growth speed | Slower | Faster |

| Formula | $SI = \frac{PRT}{100}$ | $A = P\left(1+\frac{R}{100}\right)^n$ |

| Used in | Short-term loans | Savings, investments, bank deposits |

| Interest on interest | No | Yes |

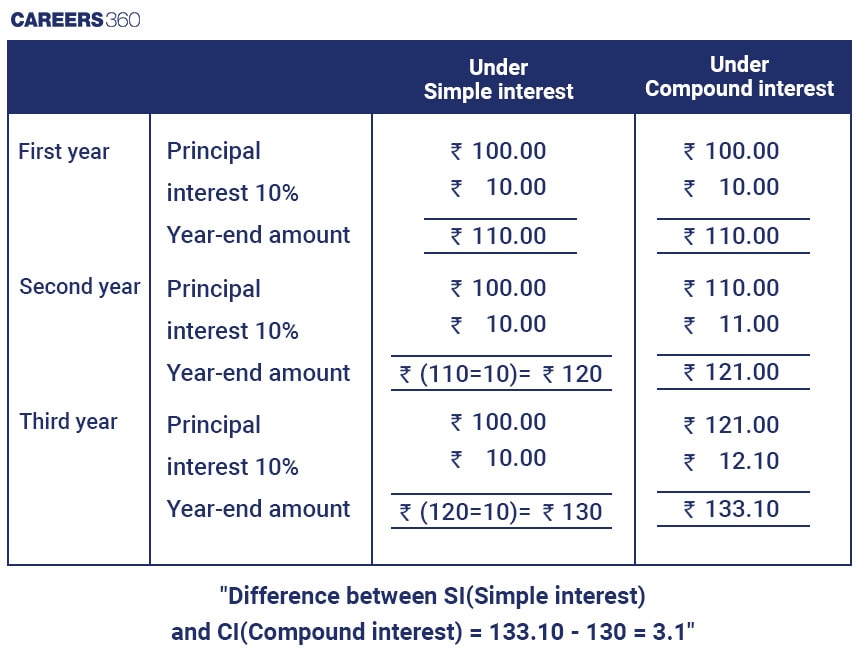

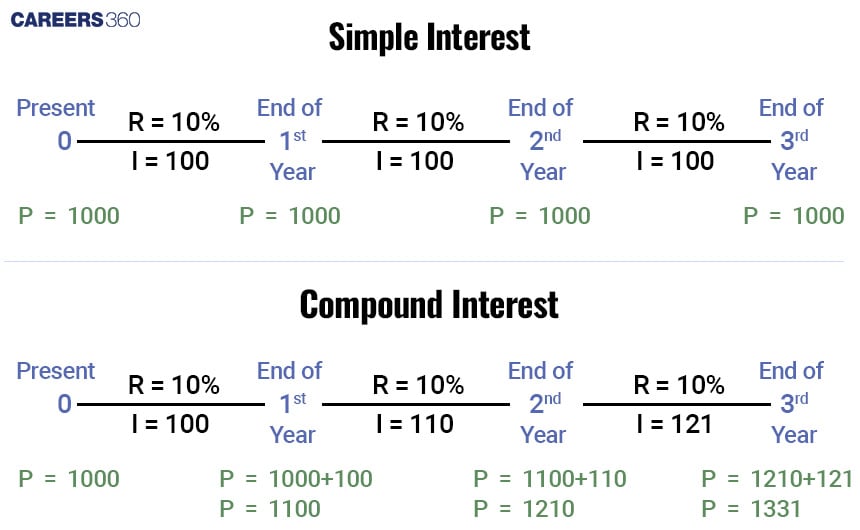

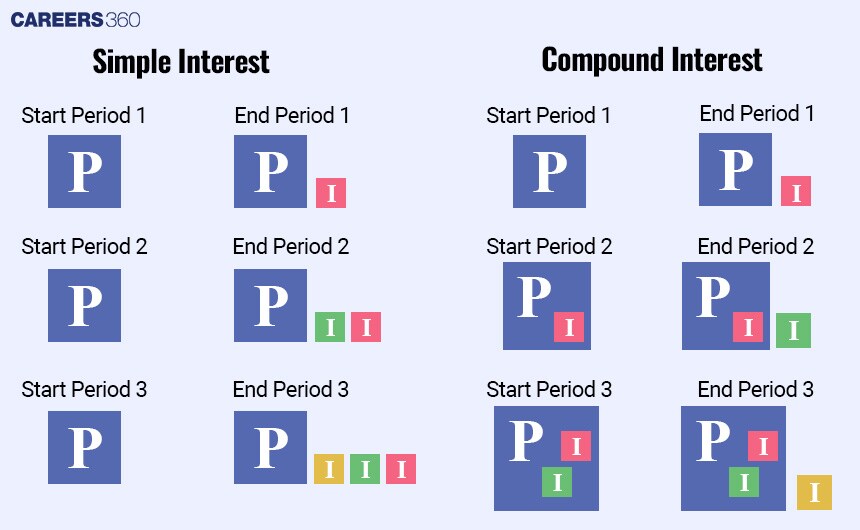

For the same amount of money for the same amount of time with the same rate of interest, if we calculate simple interest and compound interest consequently and subtract it from one another, then it is called the Difference between SI(Simple interest) and CI(Compound interest).

The below chart is an example of compound interest and simple interest for Rs. 100 for 3 years with a 10% interest rate.

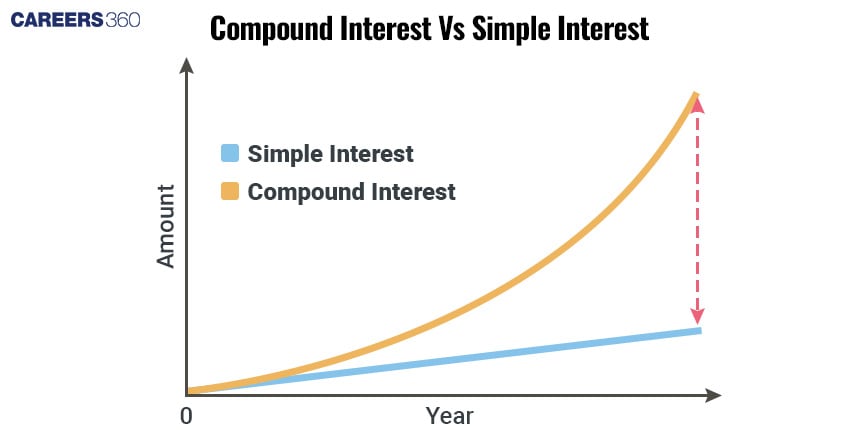

For the same principal, rate, and time, compound interest is always greater than simple interest because interest is earned on previously added interest as well.

Difference Between SI and CI for 2 Years

For 2 years, the direct formula is:

$CI - SI = P\left(\frac{R}{100}\right)^2$

Where:

- $P$ = Principal

- $R$ = Rate of interest per annum

Example

The difference between simple interest and compound interest for 2 years at 4% per annum is ₹8. Find the principal.

Using formula:

$8 = P\left(\frac{4}{100}\right)^2$

$8 = P \times \frac{16}{10000}$

$P = 5000$

Therefore, the principal is:

₹5,000

Difference Between SI and CI for 3 Years

For 3 years, the shortcut formula is:

$CI - SI = P \times \frac{(300+R)R^2}{100^3}$

Example

If the difference between CI and SI for 3 years at 10% is ₹186, find the principal.

Using formula:

$186 = P \times \frac{(300+10)\times10^2}{100^3}$

$186 = P \times \frac{31000}{1000000}$

$P = 6000$

Therefore, the principal is:

₹6,000

Quick Summary

| Time | Formula for Difference Between CI and SI |

|---|---|

| 2 Years | $P\left(\frac{R}{100}\right)^2$ |

| 3 Years | $P \times \frac{(300+R)R^2}{100^3}$ |

Quick Comparison Example

If ₹10,000 is invested at 10% for 2 years:

| Type | Interest Earned | Final Amount |

|---|---|---|

| Simple Interest | ₹2,000 | ₹12,000 |

| Compound Interest | ₹2,100 | ₹12,100 |

So compound interest gives ₹100 more because interest is added back to the principal after each period.

This is why compound interest is considered one of the most important concepts in banking maths, investment planning, and competitive exam quantitative aptitude.

Example:

Example:

Find the compound interest on Rs. 2000 for 2 years at an annual interest rate of 5%.

We know that compound interest is equal to the simple interest for the 1 year if compounded annually.

So, simple interest for 1 year = $\frac{2000 × 2 × 5}{100}$ = 200

Amount after 1 year = 2000 + 200

Simple interest for next year with principal 2200,

= $\frac{2200 × 2 × 5}{100}$ = 220

So, total amount will be 2200 + 220 = 2420 after 2 years

So, compound interest = 2420 - 2000 = 420

Compound Interest Formula

The compound interest formula is used to calculate the total amount when interest is added to the principal after every compounding period. Unlike simple interest, here the interest earned also starts earning interest in the next cycle.

This formula is widely used in questions based on savings accounts, fixed deposits, investments, and loans. It is also one of the most common formulas in school Mathematics and aptitude exams.

Standard Compound Interest Formula

The standard formula to calculate compound interest is:

$A = P\left(1 + \frac{R}{100}\right)^n$

where the amount grows every year by multiplying with the factor:

$\left(1 + \frac{R}{100}\right)$

Once the amount is found, compound interest is calculated by subtracting the principal:

$CI = A - P$

This means:

- First calculate the final amount using the formula

- Then subtract the original principal

- The remaining value is compound interest

Formula for Amount in Compound Interest

The amount formula gives the total money after interest is added for a certain time period.

$A = P\left(1 + \frac{R}{100}\right)^n$

Where:

- $A$ = Amount after interest

- $P$ = Principal invested initially

- $R$ = Rate of interest per year

- $n$ = Number of years

Example

Find the amount on ₹5,000 at 10% per annum for 2 years compounded annually.

Using the formula:

$A = 5000\left(1 + \frac{10}{100}\right)^2$

$A = 5000(1.1)^2$

$A = 5000 \times 1.21$

$A = 6050$ Rs

Now compound interest:

$CI = 6050 - 5000$

$CI = 1050$ Rs

So:

- Amount = ₹6,050

- Compound Interest = ₹1,050

Meaning of Principal, Rate, Time, and Amount in the Formula

To solve compound interest questions correctly, it is important to understand each term used in the formula.

| Term | Meaning | Example |

|---|---|---|

| $P$ | Principal or original sum invested/borrowed | ₹10,000 |

| $R$ | Rate of interest per annum | 8% |

| $n$ | Time period in years | 3 years |

| $A$ | Total amount after interest | ₹12,597.12 |

| $CI$ | Compound interest earned | $A - P$ |

Quick understanding of each term

Principal $(P)$

Principal is the starting amount of money.

Examples:

- Money deposited in a bank

- Loan borrowed from a bank

- Investment made in FD or mutual fund

If you invest ₹20,000, then:

$P = 20,000$

Rate of Interest $(R)$

Rate tells how much interest is charged or earned every year in percentage.

Example:

If bank gives 7% interest annually:

$R = 7\%$

Higher rate means faster growth of money.

Time $(n)$

Time is the duration for which money remains invested or borrowed.

Examples:

- 1 year

- 2 years

- 5 years

If money is deposited for 4 years:

$n = 4$

Amount $(A)$

Amount is the total money received after adding compound interest.

It includes:

Principal + Interest

So,

$A = P + CI$

This is the final value you get at maturity.

Important Point to Remember

In most exam questions:

- If asked for total amount → use $A = P\left(1+\frac{R}{100}\right)^n$

- If asked for compound interest → use $CI = A - P$

This small distinction helps avoid mistakes in school exams and competitive aptitude questions based on compound interest formula.

Derivation of the Compound Interest Formula

The compound interest formula can be derived step by step using the concept of simple interest. For one year, simple interest and compound interest are equal. The difference starts from the second year because interest is then calculated on the principal plus previously earned interest.

Let:

- $P$ = Principal amount

- $R$ = Rate of interest per annum

- $T$ = Time in years

Step 1: Amount after 1 Year

Using the simple interest formula for one year:

$SI = \frac{PR}{100}$

Amount after 1 year:

$A_1 = P + \frac{PR}{100}$

Taking $P$ common:

$A_1 = P\left(1+\frac{R}{100}\right)$

This amount becomes the principal for the next year.

Step 2: Amount after 2 Years

In the second year, interest is calculated on:

$P\left(1+\frac{R}{100}\right)$

So amount after 2 years becomes:

$A_2 = P\left(1+\frac{R}{100}\right)\left(1+\frac{R}{100}\right)$

$A_2 = P\left(1+\frac{R}{100}\right)^2$

Step 3: Amount after n Years

Continuing this pattern:

After 3 years:

$A_3 = P\left(1+\frac{R}{100}\right)^3$

Therefore, after $n$ years:

$A = P\left(1+\frac{R}{100}\right)^n$

This is the standard formula for amount in compound interest.

Final Compound Interest Formula

Once amount is calculated:

$CI = A - P$

Substituting the value of $A$:

$CI = P\left(1+\frac{R}{100}\right)^n - P$

Formula Summary

| Quantity | Formula |

|---|---|

| Amount | $A = P\left(1+\frac{R}{100}\right)^n$ |

| Compound Interest | $CI = A - P$ |

This formula is commonly used in school mathematics, banking calculations, fixed deposits, and competitive exam quantitative aptitude questions.

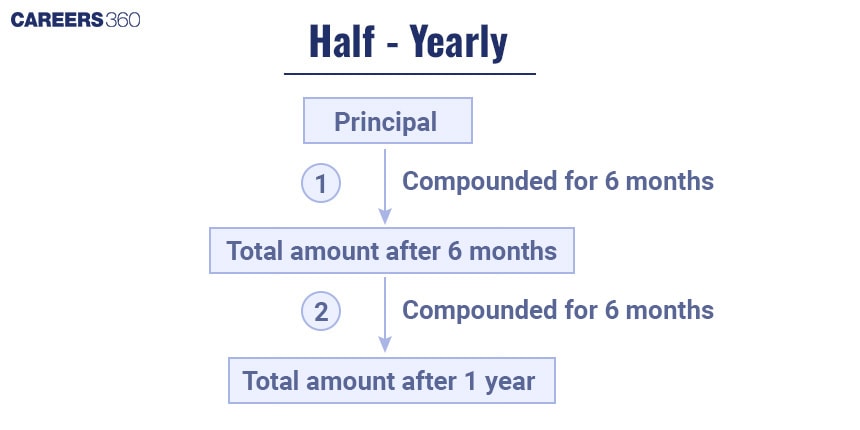

How to Calculate Compound Interest if Interest is Compounded Half-Yearly?

When interest is compounded half-yearly, it is calculated two times in a year instead of once.

Because of this:

- the annual rate of interest is divided by 2

- the number of years is multiplied by 2

Formula for Half-Yearly Compound Interest

$A = P\left(1+\frac{\frac{R}{2}}{100}\right)^{2T}$

This can also be written as:

$A = P\left(1+\frac{R}{200}\right)^{2T}$

Then,

$CI = A - P$

What Changes in Half-Yearly Compounding?

| Term | Annual Compounding | Half-Yearly Compounding |

|---|---|---|

| Rate of Interest | $R$ | $\frac{R}{2}$ |

| Time Period | $T$ | $2T$ |

Example

Find the compound interest on ₹10,000 at 8% per annum for 2 years compounded half-yearly.

Given:

$P = 10000$

$R = 8$

$T = 2$

Using formula:

$A = 10000\left(1+\frac{8}{200}\right)^4$

$A = 10000(1.04)^4$

$A = 10000 \times 1.1699$

$A \approx 11699$

Now,

$CI = 11699 - 10000$

$CI = 1699$

Important Points to Remember

For annual compounding:

$A = P\left(1+\frac{R}{100}\right)^T$

For half-yearly compounding:

$A = P\left(1+\frac{R}{200}\right)^{2T}$

- In half-yearly compound interest:

- divide rate by 2

- multiply time by 2

These formulas are frequently asked in board exams and aptitude-based exams, especially in questions based on bank interest, investments, and fixed deposits.

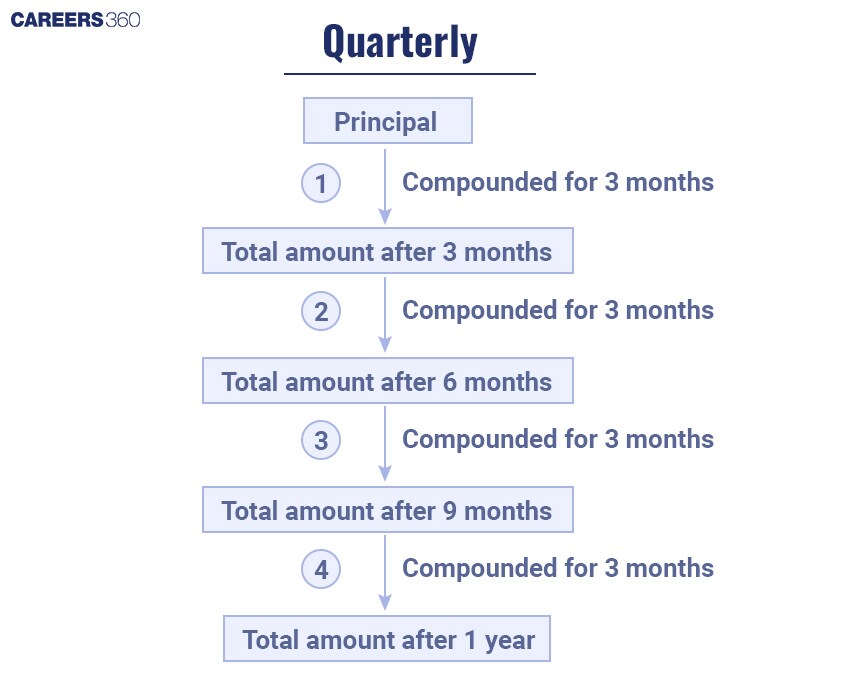

How to Calculate Compound Interest if interest is compounded/reckoned quarterly?

When compounded quarterly, interest is compounded 4 times in a year. So in the formula, the terms will be 4. Also, the rate of interest will be divided by 4, as it is compounded 4 times in a year.

When compounded quarterly, $ A= P(1+\frac{\frac{R}{4}}{100})^{nT}$,

Where A is the total amount,

P is the principal amount,

R is the rate of interest per annum, [Here Rate will be $\frac{R}{4}$]

N = Number of terms rate is compounded [Here N will be 4]

and T is the time in years.

So, final formula when compounded quarterly is $ A= P(1+\frac{\frac{R}{4}}{100})^{4T}$

How to Calculate Compound Interest if interest is compounded/reckoned monthly?

When compounded monthly, interest is compounded 12 times in a year. So in the formula, the terms will be 12. Also, the rate of interest will be divided by 12, as it is compounded 12 times in a year.

When compounded monthly, $ A= P(1+\frac{\frac{R}{12}}{100})^{nT}$,

Where A is the total amount,

P is the principal amount,

R is the rate of interest per annum, [Here Rate will be $\frac{R}{12}$]

N = Number of terms rate is compounded, [Here N will be 12]

and T is the time in years.

So, final formula when compounded monthly is $ A= P(1+\frac{\frac{R}{12}}{100})^{12T}$

Applications of Compound Interest

Compound interest is not limited to bank interest and savings accounts. The same formula is also used in many real-life calculations such as depreciation of assets and population growth or decline.

Because it works on repeated percentage increase or decrease over time, compound interest becomes useful in many practical maths problems.

Some common applications include:

- depreciation in value of cars, furniture, machines, and buildings

- population increase in cities or villages

- population decrease due to migration or other reasons

- investment growth

- loan calculations

- fixed deposits and recurring deposits

Application of Compound Interest in Depreciation

Depreciation means a decrease in value over time. Items like cars, bikes, furniture, laptops, and buildings often lose value every year due to usage, age, or wear and tear.

This decrease can be calculated using the compound interest formula with a minus sign.

Depreciation Formula

Value after depreciation:

$V = P\left(1-\frac{R}{100}\right)^T$

Where:

- $V$ = value after depreciation

- $P$ = original value

- $R$ = rate of depreciation

- $T$ = time in years

Here the negative sign is used because the value decreases every year.

Example: Depreciation Calculation

The price of a table depreciates by 20% every year. Its value after 2 years is ₹32,000. Find its present value.

Solution

Let present value = $x$

Rate of depreciation:

$R = 20%$

Value after 2 years:

$32000 = x\left(1-\frac{20}{100}\right)^2$

$32000 = x\left(\frac{4}{5}\right)^2$

$32000 = x(0.8)^2$

$32000 = x(0.64)$

$x = \frac{32000}{0.64}$

$x = 50000$

Therefore, the present value of the table is:

₹50,000

Application of Compound Interest in Population

Compound interest is also used in population-related maths problems. Population may increase every year due to births and development, or decrease due to migration, disasters, or other reasons.

Since the increase or decrease happens by percentage, it follows the same compound growth pattern.

Population Formula

Population after $T$ years:

$P_t = P\left(1 \pm \frac{R}{100}\right)^T$

Where:

- $P_t$ = population after time $T$

- $P$ = initial population

- $R$ = annual growth or decrease rate

- $T$ = number of years

Use:

- $+$ when population increases

- $-$ when population decreases

Quick Formula Table

| Situation | Formula |

|---|---|

| Population Increase | $P\left(1+\frac{R}{100}\right)^T$ |

| Population Decrease | $P\left(1-\frac{R}{100}\right)^T$ |

Example: Population Decrease

The population of a village decreases by 40% per year. If its population 2 years ago was 15,000, find the present population.

Solution

Given:

Initial population:

$P = 15000$

Rate:

$R = 40%$

Time:

$T = 2$

Using formula:

$P_t = 15000\left(1-\frac{40}{100}\right)^2$

$P_t = 15000\left(\frac{3}{5}\right)^2$

$P_t = 15000 \times \frac{9}{25}$

$P_t = 5400$

Therefore, the present population is:

5,400

Important Points to Remember

- Use $+$ sign when quantity increases every year

- Use $-$ sign when quantity decreases every year

Depreciation always uses:

$P\left(1-\frac{R}{100}\right)^T$

Population growth uses:

$P\left(1+\frac{R}{100}\right)^T$

Population decline uses:

$P\left(1-\frac{R}{100}\right)^T$

Best Books for Compound Interest

Choosing the right book can make compound interest much easier to understand and practice. The books below cover formulas, solved examples, shortcut methods, and exam-based questions for both school students and competitive exam aspirants.

| Book Name | Best For | Why It Helps |

|---|---|---|

| NCERT Mathematics Textbook | Class 8-10 students | Builds basic concepts of compound interest with simple examples |

| Quantitative Aptitude for Competitive Examinations | SSC, Bank, CUET, aptitude exams | Covers compound interest formulas, shortcuts, and practice questions |

| Fast Track Objective Arithmetic | Competitive exam preparation | Useful for shortcut methods and faster calculations |

| Magical Book on Quicker Maths | Shortcut learning | Good for mental maths and calculation speed |

| Objective Arithmetic | Practice questions | Helpful for exam-level MCQs and previous year problems |

Shortcut Tricks for Compound Interest

Compound interest questions can often be solved faster using shortcut methods instead of lengthy calculations. These tricks are especially helpful in aptitude exams where saving time can improve accuracy and overall score.

| Trick | Shortcut |

|---|---|

| Compound interest for 1 year | Same as simple interest |

| CI for 2 years | $CI = P\left(1+\frac{R}{100}\right)^2 - P$ |

| Difference between CI and SI for 2 years | $P\left(\frac{R}{100}\right)^2$ |

| Difference between CI and SI for 3 years | $P \times \frac{(300+R)R^2}{100^3}$ |

| Half-yearly compounding | Divide rate by 2 and multiply time by 2 |

| Quarterly compounding | Divide rate by 4 and multiply time by 4 |

| Depreciation problems | Use minus sign instead of plus |

Tips to Solve Compound Interest Questions Quickly

Compound interest becomes easy once you know what to look for in the question. These practical tips and exam hacks can help you avoid common mistakes and solve problems more quickly.

| Tip | Explanation |

|---|---|

| Read carefully whether amount or interest is asked | Many students calculate amount instead of CI |

| Check compounding period first | Annual, half-yearly, or quarterly changes the formula |

| Use direct formulas where possible | Saves time in MCQs |

| Convert percentage carefully | Example: $8% = \frac{8}{100}$ |

| Use depreciation formula for decreasing value | Useful in value-loss questions |

| Practice square and cube values | Helps in faster manual calculation |

| Use approximation for MCQs | Useful when exact calculation is lengthy |

Important Compound Interest Formula Table

Before solving questions, it is useful to keep all important compound interest formulas in one place for quick revision. The table below includes the most commonly used formulas for amount, compound interest, depreciation, population growth, and SI-CI difference.

Compound Interest Important Formula Table

| Concept | Formula |

|---|---|

| Compound Interest Formula | $CI = A - P$ |

| Amount Formula | $A = P\left(1+\frac{R}{100}\right)^T$ |

| Compound Interest (Annual) | $CI = P\left(1+\frac{R}{100}\right)^T - P$ |

| Half-Yearly Compounding | $A = P\left(1+\frac{R}{200}\right)^{2T}$ |

| Quarterly Compounding | $A = P\left(1+\frac{R}{400}\right)^{4T}$ |

| Depreciation Formula | $V = P\left(1-\frac{R}{100}\right)^T$ |

| Population Growth | $P\left(1+\frac{R}{100}\right)^T$ |

| Population Decrease | $P\left(1-\frac{R}{100}\right)^T$ |

| Difference between CI and SI (2 years) | $P\left(\frac{R}{100}\right)^2$ |

| Difference between CI and SI (3 years) | $P \times \frac{(300+R)R^2}{100^3}$ |

Solved Examples based on Compound Interest

Q1. At what time will ₹1000 become ₹1331 at 10% per annum compounded annually?

- 3

- $2\frac{1}{2}$

- 2

- $3\frac{1}{2}$

Hint:

$A = P\left(1+\frac{R}{100}\right)^n$

Solution:

Given:

$P = 1000$

$A = 1331$

$R = 10%$

Let time be $n$ years.

Using the formula:

$A = P\left(1+\frac{R}{100}\right)^n$

$1331 = 1000\left(1+\frac{10}{100}\right)^n$

$1331 = 1000\left(\frac{11}{10}\right)^n$

$\frac{1331}{1000} = \left(\frac{11}{10}\right)^n$

$\frac{11^3}{10^3} = \left(\frac{11}{10}\right)^n$

$\left(\frac{11}{10}\right)^3 = \left(\frac{11}{10}\right)^n$

Comparing powers:

$n = 3$

Correct Answer: 3 years

Q2. A man saves ₹2000 at the end of each year and invests the money at 5% compound interest. At the end of 3 years, he will have:

- ₹4305

- ₹6305

- ₹4205

- ₹2205

Hint:

$A = P\left(1+\frac{R}{100}\right)^n$

Solution:

Given:

Annual saving = ₹2000

Rate = $5%$

First ₹2000 earns interest for 2 years:

$2000\left(1+\frac{5}{100}\right)^2$

$= 2000\left(\frac{21}{20}\right)^2$

$= 2000 \times \frac{441}{400}$

$= 2205$

Second ₹2000 earns interest for 1 year:

$2000\left(1+\frac{5}{100}\right)$

$= 2000 \times 1.05$

$= 2100$

Third year's deposit:

$= 2000$

Total amount:

$2205 + 2100 + 2000$

$= 6305$

Correct Answer: ₹6,305

Q3. Find the amount that Shyam will get on ₹4096 if he gives it for 18 months at $12\frac{1}{2}%$ per annum, with interest compounded half-yearly.

- ₹5813

- ₹4515

- ₹4913

- ₹5713

Hint:

$A = P\left(1+\frac{R/2}{100}\right)^{2T}$

Solution:

Given:

$P = 4096$

$R = 12.5%$

Time = 18 months $= \frac{3}{2}$ years

Rate per half-year:

$\frac{12.5}{2} = 6.25%$

Number of half-years:

$2 \times \frac{3}{2} = 3$

Using the formula:

$A = 4096\left(1+\frac{6.25}{100}\right)^3$

$= 4096\left(1+\frac{1}{16}\right)^3$

$= 4096\left(\frac{17}{16}\right)^3$

$= 4913$

Correct Answer: ₹4,913

Q4. The compound interest on ₹12,000 for 9 months at 20% per annum, interest being compounded quarterly is:

₹1,750

₹1,891.50

₹2,089.70

₹2,136.40

Hint:

For quarterly compounding:

$A = P\left(1+\frac{R}{400}\right)^{4T}$

Solution:

Given:

$P = 12000$

$R = 20%$

$T = \frac{9}{12} = \frac{3}{4}$ year

Rate per quarter:

$\frac{20}{4} = 5%$

Number of quarters:

$4 \times \frac{3}{4} = 3$

Using formula:

$A = 12000\left(1+\frac{5}{100}\right)^3$

$= 12000(1.05)^3$

$= 12000 \times 1.157625$

$= 13891.50$

Compound Interest:

$CI = A - P$

$= 13891.50 - 12000$

$= 1891.50$

Correct Answer: ₹1,891.50

Q5. The price of motorcycles depreciates every year by 10%. If the value of the motorcycle after 3 years is ₹36,450, what is the present value of the motorcycle?

₹45,000

₹50,000

₹48,000

₹51,000

Hint:

Use:

$V = P\left(1-\frac{R}{100}\right)^n$

Solution:

Let present value be $x$

Rate of depreciation:

$R = 10%$

Value after 3 years:

$36450 = x\left(1-\frac{10}{100}\right)^3$

$36450 = x\left(\frac{9}{10}\right)^3$

$36450 = x \times \frac{729}{1000}$

$x = \frac{36450 \times 1000}{729}$

$x = 50000$

Therefore, present value of the motorcycle:

₹50,000

Correct Answer: ₹50,000

Q6. The population of a town increases each year by 4% of its total at the beginning of the year. If the population on 1st January 2001 was 5,00,000, what was it on 1st January 2004?

562432

652432

465223

564232

Hint:

Population after $n$ years:

$P\left(1+\frac{R}{100}\right)^n$

Solution:

Given:

Initial population:

$P = 500000$

Rate:

$R = 4%$

Time:

$n = 3$ years

Using formula:

$P = 500000\left(1+\frac{4}{100}\right)^3$

$= 500000\left(\frac{104}{100}\right)^3$

$= 500000(1.04)^3$

$= 500000 \times 1.124864$

$= 562432$

Therefore, population on 1st January 2004:

562432

Correct Answer: 562432

Q7. On a certain sum of money, the difference between compound interest for a year payable half-yearly and simple interest for a year is ₹180. If the rate of interest is 10%, then the sum is:

₹60,000

₹62,000

₹72,000

₹54,000

Hint:

Find SI and CI separately, then equate the difference to ₹180.

Solution:

Let principal be $P$

Simple Interest:

$SI = \frac{P \times 10 \times 1}{100}$

$= \frac{P}{10}$

For half-yearly compounding:

Rate per half-year:

$= 5%$

Number of periods:

$= 2$

Compound Interest:

$CI = P\left(1+\frac{5}{100}\right)^2 - P$

$= P(1.1025 - 1)$

$= 0.1025P$

According to question:

$CI - SI = 180$

$0.1025P - 0.10P = 180$

$0.0025P = 180$

$P = \frac{180}{0.0025}$

$P = 72000$

Correct Answer: ₹72,000

Q8. What is the compound interest earned on ₹80,000 at 40% per annum in 1 year compounded quarterly?

- ₹28,317

- ₹37,128

- ₹18,732

- ₹21,387

Hint:

Use:

$CI = P\left(1+\frac{R/4}{100}\right)^{4n}-P$

Solution:

Given:

$P = 80000$

$R = 40%$

$n = 1$ year

Rate per quarter:

$\frac{40}{4} = 10%$

Number of quarters:

$4$

Using formula:

$CI = 80000\left(1+\frac{10}{100}\right)^4 - 80000$

$= 80000(1.1)^4 - 80000$

$= 80000(1.4641) - 80000$

$= 117128 - 80000$

$= 37128$

Correct Answer: ₹37,128

Q9. An amount was lent for two years at 20% per annum compounded annually. Had the compounding been done half-yearly, the interest would have increased by ₹241. What was the amount lent?

- ₹10,000

- ₹12,000

- ₹20,000

- ₹24,000

Hint:

Find interest for annual compounding and half-yearly compounding separately, then compare.

Solution:

Let principal be $P$

For annual compounding:

$A = P\left(1+\frac{20}{100}\right)^2$

$= P(1.2)^2$

$= 1.44P$

Interest earned annually:

$= 1.44P - P$

$= 0.44P$

For half-yearly compounding:

Rate per half-year:

$= 10%$

Number of half-years:

$= 4$

Amount:

$A = P(1.1)^4$

$= 1.4641P$

Interest earned:

$= 1.4641P - P$

$= 0.4641P$

Difference given:

$0.4641P - 0.44P = 241$

$0.0241P = 241$

$P = \frac{241}{0.0241}$

$P = 10000$

Correct Answer: ₹10,000

Q10. The difference between compound interest and simple interest on ₹15,000 for 2 years is ₹96. The rate of interest per annum is:

- 6%

- 7%

- 8%

- 9%

Hint:

For 2 years:

$CI - SI = P\left(\frac{R}{100}\right)^2$

Solution:

Given:

$P = 15000$

Difference:

$D = 96$

Using formula:

$96 = 15000\left(\frac{R}{100}\right)^2$

$\left(\frac{R}{100}\right)^2 = \frac{96}{15000}$

$R^2 = \frac{96 \times 10000}{15000}$

$R^2 = 64$

$R = 8$

Therefore,

Rate of interest:

$= 8%$

Correct Answer: 8%

Related Quantitative Aptitude Topics

The following are some important quantitative aptitude topics frequently asked in aptitude, entrance, and competitive exams. Practising these concepts can help strengthen your basics and improve overall performance in mathematics.

Frequently Asked Questions (FAQs)

Compound interest is the interest calculated on both the principal amount and the previously earned interest. It is often called “interest on interest” because the interest keeps getting added to the amount over time.

When compounded annually, $ A= P(1+\frac{R}{100})^{T}$,

Where A is the total amount,

P is the principal amount,

R is the rate of interest per annum,

and T is the time in years.

It depends if you are lending money or saving money. If you are lending money, then it is not better for you, because you have to return the principal money with interest which may be compounded monthly, quarterly, half-yearly, or annually.

But if you are saving money, then it is good for you. Because you will save lots of money with interest

compounded monthly, quarterly, half-yearly, or annually.

Formula to find the difference between Compound interest and Simple interest for 2 years

= $P(\frac{R}{100})^2$, where P = Principal, R = Rate of interest

Formula to find the difference between Compound interest and Simple interest for 3 years

= $P×\frac{(300+R)R^{2}}{100^{3}}$, where P = Principal, R = Rate of interest

The formula for compound interest is:

$CI = P\left(1+\frac{R}{100}\right)^T - P$

Where:

- $P$ = Principal

- $R$ = Rate of interest

- $T$ = Time

If you want the total amount, use:

$A = P\left(1+\frac{R}{100}\right)^T$